The Canadian Tabulating Machine Company came into

being as follows. St. George Bond, a Canadian from Toronto who lived in

Philadelphia, obtained the Philadelphia franchise from Dr.. Hollerith prior to

1910. But in a year or so it went bust, to the tune of 15 or 20 thousand

dollars. As a gesture, and more or less out of sympathy, Dr. Hollerith gave

Bond a license to operate in Canada in 1910 and Bond then formed the Canadian

Company. The terms of the contract

called for a 20 per cent royalty payment on all rental revenues. The machines

wee to be supplied by Hollerith at cost and second hand machines were to be

shipped at nominal value. Larry Hubbard, who had received his training with

Hollerith in Washington was engaged to run the Company. The first order he took

was from Mr. Fletcher of the Library Bureau and the machine was installed in

Toronto in December of 1910.

Hubbard then set up an office in Montreal on St.

James Street. In 1911 he wrote one contract, in 1912 four, in 1913 three - all

of these are still users. By 1918 he had 41 customers with an annual rental of

about $60,000.

As I recall, prior to 1914 Canada was operated from

the United States as part of the territory of the Rochester agency of the ITR

Company of New York. From time to time, James, the Rochester manager, sent

salesman up to Canada to get business. The late Jack Barry perhaps spent more

time in Canada than any other IBM salesman. Mr. Barry later became Sales

Manager of the ITR division and when he died in 1929, had become the Sales

Manager for the entire Heavy Duty scale division. In 1914, when Mr. Mutton was

placed in charge of the ITR Company, the representation from Rochester was

discontinued and Mr. Mutton bought his time recorders directly from the parent

Company in Endicott. Later, when the Scale Company was also placed under Mr.

Mutton, it was recommended to Mr. Watson to get out of the plant on Royco and

Campbell Avenue and build a new one.

Mr. Mutton presented a plan to Mr. Watson of adding another story to the

plant. Mr. Watson accepted Mr. Mutton's

advice and it was only after a period of 20 years or so that the present plant

began to outgrow its usefulness.

In 1915 and 1916, and even before, competition

between the dial recorder and the time recorder was tough and considered a

serious factor in Canada. The dial

recorder was a sturdy and satisfactory machine. I found this out in spades when

I tried to trade 50 of them out of the Angus Shops of the CPR for new machines

of ours. Some of them had been in use for over 35 years and were still going

strong. The dial recorders were manufactured by the W.A. Wood Company of

Montreal. Mr. Mooser, later factory manager in Toronto built them. Mr. Mutton,

who was an astute and shrewd businessman, made strong recommendation to Mr.

Watson that the Company buy out the Wood Company factory and patents. This was

done in 1917.

During about five months of 1918, St. George Bond,

who has since died, acted as sales manager of the Tabulating Machine Division

under the late Mr. Frank Mutton. Mr. Mutton was appointed Vice President and

General Manager of the three divisions of the CTR Company of Canada and the ITR

in the summer of 1918. It was then called the Computing Tabulating and

Recording Company Limited of Canada, a name later changed to International

Business Machines Co. Limited.

To go back a year or so, by December of 1917 the

Tabulating Machine Company of Canada was unable to meet its payments for the

purchase of machines. While Mr. Watson had given Mr. Bond ample time to arrange

his finances to meet his obligations, he was unable to do so and some form of

relief had to be sought.

Mr. Watson then engineered the plan of forming a

Stock Company in Canada. This company would acquire majority rights in St. George Bond's interests in the

Tabulating Machine Company of Canada and the Davidson rights in the Computing

Scale Company of Canada for cash/stock in a new company. This was done in the

summer of 1918. During these meetings,

several amusing incidents occurred. Once, in the middle of the lawyers

wrangling about values and amounts claimed by interested parties, Mr. Mutton

demanded that the people representing the New York interests, Mr. Rogers and

Mr. Houston, meet with him outside the room on a matter of great importance.

Rogers and Houston found Mr. Mutton at the end of the corridor, seated on a

radiator with his legs crossed. His important question involved the

advisability of having his name placed on the letterhead as the General Manager

of the new Company.

In 1926 and 1927, all of the stock owned by the

public was bought up by the corporation. Rogers and St. George Bond were the

agents acting on behalf of the corporation in this transaction. Since that

date, the Canadian Company as been 100 per cent owned by the International

Business Machines Corporation of New York.

Between 1935 and 1939 the income and profits of the

Canadian Company increased 70 per cent. From 1935 to 1943 the income and

profits increased 800 per cent. While it is true that this remarkable growth

has taken place during the war years, it should not be overlooked that the

extreme confidence, both on the part of business and the Government in Ottawa,

led them to place their orders with our Company.

This confidence was based upon the performance of

the machines, as well as the character and ability of the personnel in the

Canadian organization. These people, through lean years and good years have

worked conscientiously in the building of the good name of IBM in the minds of

customers and prospects. It may also be

said that the Government, in searching for the mechanical means to fill its

needs during the war for accounting and statistical requirements has, with one

exception, considered only our Company as a source of supply.

The prestige of the Company was greatly increased by

Mr. Watson's visits to Canada prior to and following 1937. In 1937, as each

year thereafter he met the most prominent men in Canada, commercial,

educational and governmental. He also made many public addresses. On September

2nd of 1941 he took the entire executive staff of the IBM Corporation to the

Canadian National Exhibition. The Company was being honoured at the CNE's

International Day. That evening Lily Pons and Lawrence Tibbett gave a concert

at the Band Shell in front of some 60,000 people. This large audience was addressed by Mr. Watson, Mrs. August

Belmont and myself. At that concert, a generous donation of $10,000 went from the Company to the Canadian Red

Cross to help in the war effort. While this large sum was given without

publicity, the kind comments of the officer and directors of the Red Cross

would have been heart warming to any IBM executives, could they have heard

them.

During Mr. Watson's visits many changes were made to

the form and conduct of the business. In the latter part of 1937 he purchased

the property on King Street. The executive offices were separated from the

factory and IBM executives could be at the heart of the city's financial

district.

In the very early days, there were only three employees

of the Company, all located in an office at 15 Alice Street. I believe that

Alice Street became Teraulay Street and the original site is now a parking lot.

In December of 1938 Mr. Watson purchased the Beaver Hall property and the

office building erected on this site is considered to be the most modern of its

kind in Canada. Having one of the Company's executives living in Ottawa where

he could mix it up with the various government departments and personnel from

1935 onwards also helped the Company build up its business in Canada.

Another factor which had a lot to do with the

welding of the Company personnel into a

united team was Mr. Watson's authorization for the purchase of a country club.

This property, purchased in 1942, consists of 100 acres just outside the city

limits. It's fully equipped and has a play house and playgrounds so that the

entire family can enjoy themselves. Mr. Watson authorized the purchase of an

additional 100 acres adjacent to the Country Club. This property crosses the

main feeder line for the CNR and will make a suitable site for a manufacturing

plant as and when needed in the future. It is cheap land at the price and is

currently being farmed by the farmer who sold it to us, on an annual rental

basis.

The

Story of the British War Orphans

Following the German invasion of France in May and

June of 1940, when England was in great danger, Mr. Watson, with characteristic

thoughtfulness for others, cabled

Stafford Howard, Managing Director of the ITR in London, inviting the

wives and children of employees to take refuge in Canada at the Company's

expense.

In response, nine mothers and nineteen children

arrived in Toronto on July 5th 1940. This first group was followed by a second group of three mothers

and four children on October 9th of the same year. They were

temporarily housed at the Sisters of St. John the Devine hostel at 49 Brunswick

Street in Toronto.

Mr. Watson then authorized the purchase of lake

frontage at Bronte, about 28 miles west of Toronto. This property consisted of

eight acres, including fruit and market garden and two fine houses. When Mr.

Watson and Mr. Nichol visited Toronto on July 15th, 1940 to inspect

the property, and make the necessary arrangements, certain reservations on the

part of some of the evacuees caused him to abandon his plan - and the property

was sold without loss.

The evacuees were the lodged in boarding houses in

the west end of Toronto and suitable arrangements were made for schooling etc. Now that return permits

are being granted by the British government, some of our families have returned

home and there will no doubt be others in the near future.

The policy inaugurated by Mr. Watson to encourage

employees to mix in community affairs and join business and trade associations

has had much to do with establishing the prestige and reputation of our Company, as well as the development of

the individual. The Company's employees represent a standard of intelligence

and character which fits them all for such a roll. The very nature of the business

permits and demands constant development along business lines. This is

characteristic of the successful IBM man and stamps him with qualities of

leadership, both in public speaking and leadership. He attracts attention

wherever businessmen gather.

In the United States and Canada you will find IBM

men in the forefront of sales executives' clubs chambers of commerce,

manufacturers associations and boards of trade. Honours and preferments seem to

come to them naturally. This is the natural product of the educational system

fostered and promoted by Mr. Watson. The Company is no place for the bounder or

the philanderer. We have had some in the business, but they don't stick.

At the time when Mr. Watson took over the management

of the CTR Company in 1914, it is safe to say that every member of the sales

force of the CTR thought that the Company was on the upswing of an unending

period of growth, and the equipment consisting of the No. 15 Key Punch, hard

punch, vertical sorter and the non-automatic, non-lister tabulator would do the

trick.

As a matter of fact, the initial impetus given the

business when Dr. Hollerith installed the large machines with the Railway and

Insurance companies, was petering out and the Company was running into shallow

waters. The progress made in the book

keeping, adding and listing machines, and the improvements made by a competitor

with a similar machine, was bidding fair to eliminate us as a serious

competitor in the office specialty field.

The Company was going down hill instead of up and if

it had not been for the new machines which the Engineering and research

Departments had developed under Mr. Watson, the Company would have been limited

to certain kinds of statistical work. These new machines such as the Horizontal

high speed sorter, Printing Tabulator with Automatic Group Control, Electric

Key Punches and many other devices, have made possible the growth of the

Company.

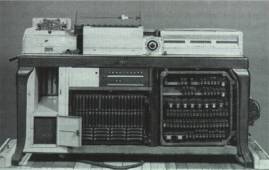

An early

combined tabulator/sorter

Concurrently with the improved machines, the sales

department was increased. All salesmen participated in a comprehensive

educational system on our products. A refresher course for the older salesmen

was also developed.

The Company had a new birth and was ready for larger

service to the business world, beyond the dreams of the original founders of

the Company.

The

Story of Tauschek in Europe

The advent of Tauschek into the electrical

accounting field makes interesting reading.

Tauschek, a young Austrian living in Vienna, was a

clerk in a bank in Vienna in 1926 or 1927 or perhaps earlier. One of the

clients of the bank was the Powers Accounting Company. One of Tauschek's duties

at the bank was to scrutinize cheques, including those from the Powers

Accounting Company. In the case of the Powers Company, two signatures were

required.

On one occasion, Tauschek failed to note that only

signature was on a cheque destined for New York. The cheque came back and Tauschek took it over to the Power's

office to have it signed. Tauschek had never seen Power's accounting machines

and he asked the company manager explain to the machines to him.

Tauschek made

one or two visits to get additional information, and in the course of

conversation, he found that the mechanical tabulating machines were being sold

in Europe for between $15,000 - $20,000. Tauschek decided that the price was

too high and that a cheaper machine could be built which would do the same

work.

He then got in touch with patent offices in Germany,

Great Britain and the United States. Tauschek had copies of all patents which

had been issued concerning tabulating machines sent to him. He then took a

course in English so that he could read and comprehend all the material.

As a result of investigations, research and model

building, he secured patents from German, Great Britain and the United States

in and around existing patents. He then manufactured a model key punching

machine, a sorter and a tabulating machine, the principles of which were

slightly different from the existing types.

With this beginning, Tauschek entered into a

contract with the Rhein Metalls Company to develop his patents and build the

machines for commercial use. This contract was entered into around 1929.

Dehomag, our German subsidiary, was somewhat

disturbed by Tauschek as a potential competitor and was in favour of

negotiating with him.

During a trip to Europe in 1929, Mr. Watson had

Rottke (of Dehomag) and Tauschek come to London, to meet with himself, Mr. Jennings and myself (as

the newly appointed European General Manager).

The negotiations were held in Grosvenor House in London. After a week of

negotiating the IBM Company bought out

Tauschek's patents, and the models he had developed, with the exception of one

set of machines which Tauschek presented to the Vienna museum. As well, Tauschek secured five years of

employment with IBM, seven months of each year to be spent at the IBM labs in

the United States. As additional consideration, Tauschek also agreed to

unreservedly convey all his ideas and patents with regards to electric

accounting machines.

At about the time of the end of his contract with

IBM, it was discovered that he had proceeded with certain patents secretly

concerning the development of an electric eye principle. He had not turned this

work over to IBM, as per the terms of his agreement with us. Tauschek was

brought sharply to task by the Company but it began to look as if the only way

the Company could get redress would have been through the courts. In the midst

of negotiations, he fled, returning illegally to Germany. The rumour was that

he had been called back to Germany to complete work on a new type of machine

gun that he had developed for the German government.

There are a number of reasons which led up to the

increase of the capital structure and the consolidation of the three companies

in Germany: Dehomag, Ingemag (the scale company) and the Sindelfingen Scale

Factory. The capital of these companies

was nominal. I think that Dehomag's amounted to something like 300,000 marks.

We had kept the capital of the companies low on purpose, because the German

government taxed on capital stock. In fact, the two scale companies had never

shown a profit. Dehomag was different though and in 1932 and 1933 its profits

soared to four and five times its capitalization. The German Treasury began

careful scrutiny of firms such ours and of course this scrutiny was aided by

supplementary information provided by Nazi observers. The observers were

assigned by party leaders to all industrial plants throughout Germany. There

was always one observer keeping track of things and in some cases two or three,

depending on the size of the plant.

Dancing

With the Devil - Nazis On Staff

At Dehomag we had a young Nazi by the name of

Fredericks who was on staff as an 'observer'.

I learned that Fredericks was one of the party of six Nazis who broke

into General Von Schleicher's residence during the infamous June, 1934 "Night of the Long Knives" purge

of Ernst Rohm and others.

General Von Schleicher

General Von Schleicher

Fredericks and the others executed Von Schleicher

and his wife in cold blood.

The fact that Dehomag was paying out annual

dividends many times the amount of its capital had resulted in certain

questions being asked by the German Treasury. At the same time, the Dehomag

Company had been made the target of abuse and criticism from the Nazi

controlled press throughout Germany on the grounds that the use of Dehomag

electric accounting machines threw clerks out of work. In government offices in

Hanover in 1932 civil service employees went on a bit of a rampage and

partially destroyed their newly installed Dehomag machines. This incident

received widespread publicity.

About this time our agent in Munich, a Mr.

Pappenburg had caused Rottke and Heidinger some concern due to reports coming

in to the Munich office concerning Pappenburg's unexplained absences from

work. They asked me if it would be all

right if they put a 'tail' on Pappenburg. As they seemed quite worried, I

agreed to their request. The reports we got back showed that Pappenburg was a

very active Nazi and that his absences were due to his attendance at various

conferences and meetings of the Nazi party. This gave Mr. Heidinger the idea of

using Pappenburg to meet Hitler at Hitler's Nazi headquarters. He wanted to

establish friendly relations with Hitler and the Nazi party so that the party

would discontinue its attacks on Dehomag. It is my understanding that Heidinger

became a Nazi party member at the meeting.

The result of this meeting relieved the Company from

further investigation by the German government and hostile criticism of the

Company by the Nazi controlled press stopped. In addition, the capitalization

of the German companies was increased to 7,000,000 marks. All the losses at the

Sindelfingen plant and at Ingomag were also capitalized. Over the next period of time, Dehomag and

the Sindelfingen plant became the only active units in Germany. The Small Scale

Factory (Ingomag) gradually folded. Interestingly, in 1934 the output of the

Sindelfingen plant was 85 per cent weaving machines - most of which were sold

to the Russian and German armies for the making of military uniforms.

Mr. Rottke did not become a Nazi until 1933. In the

fall of that year I called a meeting in Paris of all European managers which

Mr.Rottke attended. During the meeting Mr. Rottke took me to one side and said

that a demand had been served on him by the Nazi Party to become a member. He

wanted my advice and he showed me the letter and stamped self addressed

envelope that the Nazis had given him. He told me that he had been given 24

hours in which to answer their demands. From his manner, I surmised that he was

hoping that I would advise him not to join. But this was clearly a matter for

Rottke and his family to decide, on their own. I understand that he mailed his

application to join the Nazi Party the next morning.

Collecting delinquent ITR and EAM accounts was a bit

different from collecting delinquent accounts in other businesses due to the

close and continuing relationship that existed between the Company and its

customers. Instead of pressure letters and calls from lawyers representing the

interests of head office, it was customary to have the EAM Manager or salesman

assume the role of bill collector when an account was past due.

This often placed our representatives in a difficult

position and frequent dunning calls to collect the money did not tend to

improve his standing with his customers.

Coming out of the twenties, there were a great

number of EAM customers who were delinquent. In addition, the accounts with the

government in Washington had become hopelessly in arrears for a number of

reasons, one of which was the failure of the billing department to put in

sufficient information to allow proper accounting to be made for the public

monies expended. Something had to be

done and it was decided to make a change.

The late W. C. Sieberg, who was the General

Bookkeeper of the EAM Division, was given the job. His first task was to straighten

out the Washington situation and then he was to move on and clean up the rest

of the accounts throughout the country.

Mr. Sieberg spent about four months in Washington and got the Government

accounts up to date. At the same time that Mr. Sieberg was chasing down delinquent customers, we brought in Mr.

Brown to do Sieberg's old job. Brown had been an accountant at a factory and we

brought him in so that he would gain a thorough knowledge of head office accounting,

which he could then take back to the

factory.

By way of commentary, it is my opinion that a good

EAM accountant, of broad commercial training, should always work as the liaison

man for the collection of delinquent accounts, rather than depending on the

salesman to do the collecting. The Company has ever, to my knowledge prosecuted

a customer for the non-payment of an account. Hence, it becomes a matter of how

and when to make a compromise agreement or settlement with a customer.

To an ingenious negotiator, it is almost always

possible to effect some form of agreement to protect the Company's interests,

and to ensure that the customer does not disregard his obligations to pay. In

certain cases, treasury stock or bonds have been accepted. I cite the case of a

Canadian aircraft company who was in arrears for over 18 months in 1936 and

1937. I interviewed the Treasurer of the company and we reached an agreement

whereby they would pay us monthly installation charges and the balance would be

held in suspense until they were able to make payments on the old balance. Any

payments made by the company were applied against the oldest balances. Within

two and a half years the account was brought up to date and it has not been

delinquent since.

A

Historical Note on the Bull Company

It would seem proper to have some reference in the

historical data about the development of the Bull machine. The following is a

very sketchy outline and it should be supplemented by more accurate and

detailed information.

Dr. Fredrik Rosing Bull, a Norwegian, developed the

machines. When he died, he left his plans, his notes and diaries and the

machine's specifications

Dr. Bull

Dr. Bull

and whatever patents he had, to the University of

Oslo where they lay dormant for a number of years.

Emile

Genon, who later became our agent for Belgium, had been in the office specialty

business for years as a Belgian reseller of Elliott-Fisher and Underwood

calculators. In the course of his travels, he found out about Dr. Bull's

machines and that the University of Oslo had done nothing with them. Genon saw

possibilities. He got a group of interested investors together in Paris.

Members of this group included the auditor for the French Railway (a large

customer of ours) and general in the French army. Genon got enough money together to purchase all rights pertaining

to the Bull machines (except for Scandanavia) from the University of Oslo. As I

recall, Genon told me that he was able to buy these rights for $10,000.

The models were shipped to Paris, and under the

General's supervision, a limited number were built and installed in customer's

offices. According to all reports, they worked quite well. The Sorter was of the horizontal type and

was unusually light, in fact, about half the weight of our machine. The

Tabulator-Printer had a speed of about 230 cards per minute for listing and

adding. The type bar was of the rotary

principle. Under Genon's management, the Bull Company bid fair to make inroads

on the established business of the

Company.

At my suggestion, Dehomag sent two of their representatives

to investigate the machines. These representatives reported to Heidinger and

Rottke that the machines had considerable merit. The Bull machines were

demonstrated at the Paris Exposition in 1931 and attracted considerable

attention.

With this background, when Mr. Braitmayer visited

Europe in 1933, arrangements were made for him to meet with the Bull group in

Paris, and certain tentative negotiations were carried on in a regard to a

possible acquisition by our Company of the Bull Company

Genon

was later employed by our Company as our representative in Belgium. In November

of 1935 IBM Mr. Watson proposed to buy

all Bull assets for 2.8MF (including patents). In December of 1935 Emile Genon transferred 86% of Bull AG to IBM.

The next day, the Callies family proposed a new stock subscription of 6MF,

approved by Marcel Bassot, to avoid an IBM take over.

Costs

and Profitability During the War

On March 2, 1943 the Canadian Company was asked by

the Department of Munitions and Supply to submit a statement of income, costs

and profit on any installations that might be considered war business with the

Department. This request was later broadened to include all government business

which could be classified as war business. The object of the inquiry was to renegotiate

our contracts with all government departments to establish fair and reasonable

profits on installations arising out of the war and to arrive at the portion of

the profit to be refunded.

At that time, the Canadian Company purchased EAM

equipment from the Parent Company on the basis of flat factory cost. We

therefore brought to the attention of Department officials that we were unable

to submit an accurate statement of costs. This flat factory cost did not

include administrative overhead, the costs of engineering, patents, development

or research. The Department indicated that it would be perfectly reasonable to

include any such items in our estimate of our costs and that the Department

wold have the right to scrutinize such items to determine whether they were

fair and reasonable.

On June 4, 1943 our Controller, A. L. Williams,

furnished a statement that showed the amount of such expenses, applicable to

the Canadian Company, expressed in terms of per cent, would approximate 5 per

cent of the total revenue of the Canadian Company for the year 1942.

The increase in cost of the over-all picture of the

Canadian Company, had the expense been included, would have amounted to

$167,687 (Gross Canadian income - $3,563,917) of which about $50,000 would be the

amount to be added to the cost of our war installations with the Government.

(Government installations in round figures, $1,000,000 per year or

approximately 25 per cent of total installations).

In view of the known losses we would sustain when

the war ended by discontinuances and cancellations, plus the unamortized value

of the machines which would be returned to us, I did not consider that the

figures being presented were fair for the Company. It was not enough for us

just to build up our cost figures.

I therefore decided to fight for the inclusion in

our costs of the 25 per cent royalty paid by other subsidiary companies. We were finally able to convince Department

officials to agree to the inclusion of this 25 per cent fee and an agreement

was reached by May of this year (1944).

On $1,000,000 of revenue, the royalty cost will amount to $250,000 as

against $50,000 had we decided to include IBM Corporation overhead as an item

of cost.

Historical

Data - Census Machines

Perforated papers and cards were used to select and

control patterns in the weaving industry in the eighteenth century. This

principle was improved by Joseph-Marie Jacquard, a French inventor of Lyons

prior to 1806. The introduction of these 'Jacquard Looms' caused riots against

the replacement of people by machines.

Babbage

Babbage

It remained for Charles Babbage, an English

mechanic/mathematician to experiment with the principle of punched holes in

relation to a calculating machine. Babbage got government support for his

machine in 1822, but his 'Difference Machine' was never completed.

In the 1850's and 1860's, the development and use of

punched holes in paper for player pianos and organs was a great commercial

success.

It is perhaps with some of this background in mind

that Dr. Hollerith seriously considered adapting the principle of punch cards

for the compilation of the US census of 1860, from a chance remark made to him

by a young woman. He had been called to Washington in the early '80s to act as

a special agent in the Census Department. During a pleasure cruise on the

Potomac with Census Department co-workers, a young woman asked Hollerith:

"Why don't some of you men devise a card for the census work by punching

holes into it and making a machine do the rest of the work?"

By 1889 Dr. Hollerith had perfected and patented a

card with 12 rows of 20 positions for holes, to be punched on a Pantagraph

Keyboard Punch. His tabulator was similar to a printing press with the cards

being fed by hand and a handle which operated the press, thus allowing the pins

to press through the card. Wherever these pins went through the hole in the

card, electrical contact was made in a mercury cell below. The result was

registered in one of forty different counters. An attached sorting machine

consisted of a horizontal box with two rows of thirteen compartments, Each

compartment had a lid controlled by a magnet. This machine was controlled by

wires from the tabulator. To prepare for the next sort, the operator removed

the card from the tabulator and dropped the card into the compartment through

which the tabulator had just sent an impulse to cause the lid to open. The

compartment lid was then closed by the operator.

In April of 1889 a Commission was formed to advise

Mr. Porter, Superintendent of the US Census, as to the methods to adopt of

tabulating census data. To this Commission, three schemes were presented. Mr.

Hunt's scheme proposed to transfer the details given on the census enumerator's

schedules to cards, distinctions being made in part by the color of ink, and in

part by written notations, the results being reached afterwards by hand sorting

and counting. Mr. Pidgin proposed a scheme whereby chips would be used. These

chips could then be duly sorted and counted by hand. Mr. Herman Hollerith then

made his presentation, described above.

The three proposals were then put to the test in

four enumeration districts in St. Louis. It was found that the time occupied in

transcribing the enumerator's work (10,491 inhabitants) by the Hollerith method

was 72 hours and 27 minutes. The Hunt method took 144 hours and 25 minutes, Mr.

Pidgin's plan took 110 hours 56 minutes. He time occupied in tabulating was

found to be as follows:

·

Hollerith's

electrical counters - 5 hours 28 minutes

·

Hunt's

slips - 55 hours, 22 minutes

·

Pidgin's

chips - 44 hours, 41 minutes.

That settled it. Hollerith got the contact. The

Commission also estimated that based on America's population of 65,000,000, the

savings with the Hollerith machines wold amount to over $600,000. As a matter

for the record, that estimate was based on an average of 500 cards punched per

day, while 700 per day turned out to be the average - the savings were 40 per

cent more than expected. By way of contrast,

the work of tabulating the 1890 census was finished in ten months. The previous

census, undertaken in 1880, still was not fully tabulated when the 1890 census

began. In fact, some of the data from the 1880 census was never tabulated -

this despite a workforce of 47,950

women tabulators working in the daytime and 32,935 men tabulators working at

night (figures from "Electrical Engineer", November 11, 1891 pp.

522).

Dr. Hollerith's connection with the U.S. Census

Department did not continue very much longer after the completion of the 1890

census. The relations were broken, as I understand it, through differences that

arose between himself and government officials or official. He withdrew and the

department started to build its own machines, incorporating the Hollerith

principles in the machines that they built. James Powers, a foreman in the

Census Department, developed a key punch which the Department adopted. Mr.

Powers, of Jewish origin, continued his developments and research work with the

result that he developed a horizontal sorter and printer-tabulator, both

mechanical, on which no patents had been taken out by Dr. Hollerith. Dr.

Hollerith had considered three methods for a power supply when he perfected his

machine; electrical, mechanical and compressed air. He took his patents out on

the electrical method - leaving others the option of developing machines with

compressed air or mechanical power.

This was the start of the Powers accounting machine.

Dr. Hollerith went on to assist in the census

processing for many countries around the world. The company he founded,

Hollerith Tabulating Company, eventually became one of the three that composed

the Calculating-Tabulating-Recording (C-T-R) company in 1914, and eventually

was renamed IBM in 1924.